Measuring Productivity in the Workplace

Types of productivity measures include:

Capital productivity is used to measure how efficiently a business utilises physical capital to produce goods and services. Physical capital refers to tangible items such as labour, materials, warehouse supplies, computers, and vehicles – items used to create products. Capital productivity is calculated by subtracting liabilities from physical capital and then dividing sales by that number.

Material productivity is used by businesses that provide services, rather than products. Material productivity is calculated by subtracting liabilities from material capital (natural resources) and then dividing sales by that number.

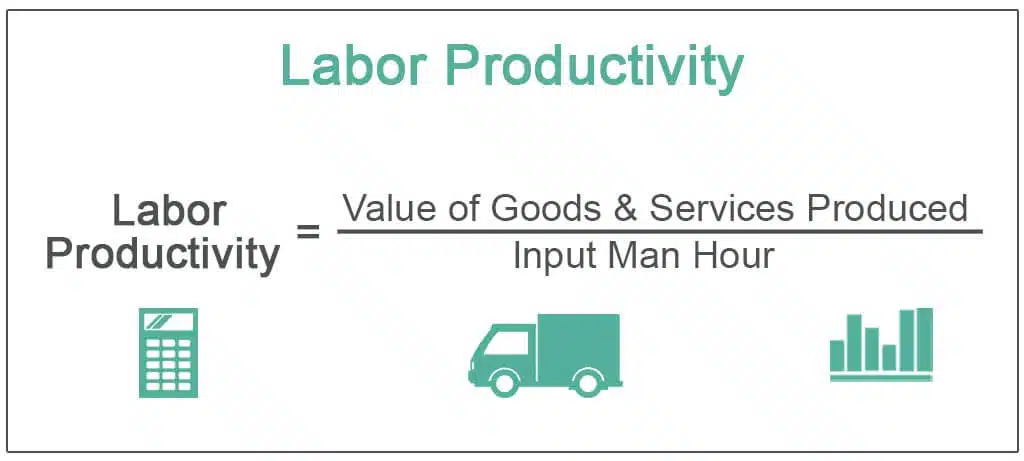

Labour productivity measures how productive each employee is. It considers the ratio of output per person. It is calculated by dividing the value of goods/services by the number of hours employees took to make them.

Total factor productivity looks at production levels using the weighted average of labour and capital. It is calculated by dividing the total production by the weighted average of time and capital. Total factor productivity focuses on the effect of labour and capital.